Selling the oil and gas

The Valhall partners entered into an agreement to share revenues from oil and gas sales on the basis of their proportionate interest in the field.

Crude oil was initially sold under contracts with specific customers which specified the quantity to be delivered, the time of delivery, and the price to be paid. But it was swiftly discovered that this approach failed to optimise profit. The spot market, where individual tanker cargoes are sold to the highest bidder, was more profitable – but more demanding.

Contract sales ensure stable prices, because specified quantities are negotiated at a fixed rate over a lengthy period – months or years, as is common in the Middle East, for example.

Oil sold spot often earns more because of the ability this approach provides to take advantage of fluctuations in both prices and demand. Like most of the oils from the North Sea, Valhall crude is a particularly attractive grade in terms of its product specifications. That has meant it is in demand both as a main product and for blending with cheaper grades with less attractive qualities, such as heavier oils from the Middle East.

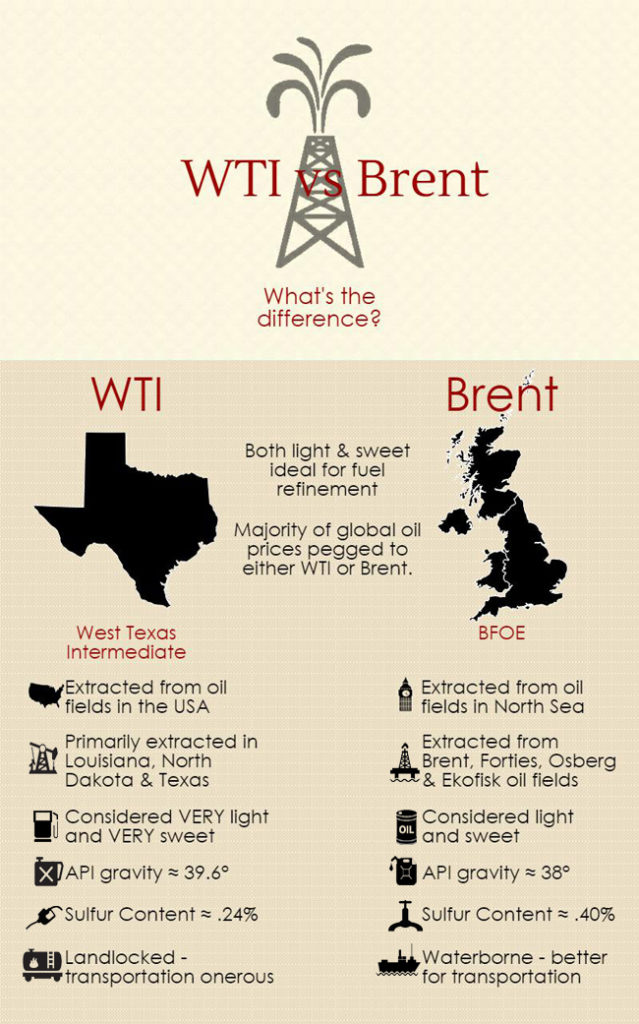

Two terms are important for determining spot prices – the cost of Brent Blend “reference” crude and the divergence in quality from this grade.

Salg av olje og gass

Salg av olje og gassBrent Blend is priced daily by independent publications in London, and the market price is typically the average of this rate on the day the oil is loaded into tankers and for two days before and after – in other words, an average of five days.

The quality difference is the supplement or deduction determined by negotiations on the basis of quality, quantity and the buyer’s requirements.

Valhall oil is sold in practice when it leaves field, which means that the individual partners cease to own the crude once it has been pumped into the Norpipe line to Teesside in the UK.

Another reference price is the one used in the USA – West Texas Intermediate (WTI). Like Brent Blend, this is set by independent pricing publications on the basis of WTI sales. For a long time, the relationship between these two guideline prices was based – as a rule of thumb – on freight costs between Europe and the USA, with WTI having the higher value.

Gas sales

Gas has been used in many European countries since the 19th century. But it was not until the 1960s – when the Netherlands began production and export from its big Groningen field – that a common market for this commodity began to develop in Europe. The Soviet Union, Algeria and Norway gradually followed as gas exporters in the 1970s and 1980s, developing infrastructure for production, transport, storage and consumption as demand grew. Establishing a system of pipelines from fields in the producer countries to the minor distributors called for heavy investment, which needed to be repaid. To ensure that, long-term contracts usually lasting for 20 years were established between the gas producers and the transmission companies in the consumer countries.

Salg av olje og gass

Salg av olje og gassNorwegian gas exports began with the development of the Ekofisk area of the North Sea and the construction of a pipeline to Emden in Germany, which became operational in 1977. After tough negotiations, Valhall gas was also piped via Ekofisk to the same destination for distribution to industry and households in Germany, the Netherlands, Belgium and France.

In 1986, the Norwegian government established a gas negotiating committee (GFU) to handle the preparation and conduct of all discussions on gas sales from licences awarded after 1985. This body comprised representatives from Statoil, Norsk Hydro and – until 1999 – Saga Petroleum. They were supported in individual negotiations by personnel from foreign companies. Should licensees be able to achieve better terms or market the gas to their own facilities, they could reach sales agreements independently of the GFU.

But the government opted to end this arrangement in 2001, since it conflicted with the EU’s gas directive and competition rules. Sales of Norwegian gas through the GFU to the European Economic Area (EEA) were finally terminated on 1 January 2002.[REMOVE]Fotnote: Store Norske Leksikon.

Salg av olje og gass

Salg av olje og gassGassco ensures that Norwegian gas is delivered to continental Europe and the UK, where it meets almost 20 per cent of consumption of this commodity. Established by the Ministry of Petroleum and Energy on 14 May 2001, Gassco is responsible today for transporting all gas sold by licensees on the Norwegian continental shelf (NCS).

This state-owned company took over operator responsibility for most pipeline systems from the NCS on 1 January 2002. Before that, these facilities had been operated by several companies. Creating Gassco was part of an extensive restructuring of Norway’s petroleum sector around 2001, and met the EU’s requirements as specified in the gas market directive.

The political reasons for the company’s establishment found expression in Proposition (Bill) no 36 to the Storting (2000-2001) and Recommendation no 198 (2000-2001) from the Storting (parliamentary) committee on energy and the environment.

These specified in part that Norway’s transport and treatment facilities must serve all gas producers equally, and that Gassco would be neutral in relation to these players.

Salg av olje og gass

Salg av olje og gassDuring the company’s first year of operation, the gas transport system was opened to third parties as required under the EU gas directive. With the GFU also wound up, marketing and sale of Norwegian gas became the responsibility of the individual producer companies. The Gassled joint venture was established by merging several earlier pipeline partnerships, and took over as the formal owner of most Norwegian gas infrastructure.[REMOVE]Fotnote: www.gassco.no/om-gassco/historie/