Rows over royalties

For many years, royalty payments had been a good source of revenue for the government and a corresponding expense for the companies. The question is what disputes actually arose over them, and why it took so many years to find a resolution.

This story begins with Norway’s first offshore licensing round in 1965, when the blocks in which Valhall was eventually discovered were awarded.

The government made money from these allocations through various duties – the one-off fee or lump sum , an annual area fee if the licence was retained beyond six years, and a production fee or royalty. (See the article on AmocoNoco group seeks licences.)

Avgifter til besvær, økonomi og samfunn,

Avgifter til besvær, økonomi og samfunn,The annual area fee was paid for permission to pursue exploration for or production of petroleum resources in a defined part of the Norwegian continental shelf (NCS).

This payment was initially fixed for an exploration period limited to six years, and then increased on a linear basis over 10 years. It was specified in 1965 to rise from NOK 500 per square kilometre to a maximum of NOK 5 000 – an amount which was adjusted upwards over time.

Deductible from taxable income, the area fee was intended to help ensure that licensed areas were explored efficiently and that discoveries were brought on stream swiftly.[REMOVE]Fotnote: Letter from the Norwegian Petroleum Directorate (NPD) to the Ministry of Petroleum and Energy, 17 October 2006.

Its purpose was also to encourage companies to relinquish acreage they did not consider commercial, so that new licensees could eventually be given a chance to explore there.

The production fee was set in 1965 at 10 per cent of the gross value of the oil and gas produced, with no deduction of operating and investment costs.

Differentiated rates were introduced in 1972, when the fee was officially renamed as royalty. These varied from eight to 16 per cent for oil and amounted to 12.5 per cent for gas.

The system was amended again as part of tax reliefs for the oil companies after the price slump in 1985-86, with royalty being scrapped for licences awarded after 1986. And another fiscal reform in 1992 saw it abolished for gas from older fields.[REMOVE]Fotnote: Norwegian Official Reports (NOU) 2000:18 Skattlegging av petroleumsvirksomheten.

Deadline for royalty payments

Avgifter til besvær, økonomi og samfunn,

Avgifter til besvær, økonomi og samfunn,The oil companies did not react until licence terms were revised in a more rigorous direction in 1972, when payment provisions were among the bones of contention.

It had been specified in 1965 that royalty should be paid at six-monthly intervals and within three months from the end of each biannual period.

The 1972 regulations changed this to a quarterly settlement within 30 days.[REMOVE]Fotnote: Royal decree of 8 December 1972, section 26, sixth paragraph. Applied to all fields from 1 January 1977, this meant the oil companies made less money on the interest-rate margin while the government benefited.

Phillips Petroleum, fronting for nine oil companies with licences awarded in 1965, went to court in 1982 to have the revised payment scheduled clarified.

The government’s case turned out to be insufficient. Indeed, the Ministry of Petroleum and Energy had noted in its recommendations that caution should be shown in applying the new provisions to older licences.

Phillips and the other oil companies won in the Oslo District Court, and the government was forced to refund the lost interest. The case went to the Court of Appeal and the Supreme Court, which handed down its judgement on 19 December 1985.[REMOVE]Fotnote: Supreme Court judgement – Rt-1985-1355.

At each round, the outcome was the same – except that the amount to be repaid increased. It amounted to more than NOK 140 million plus legal costs for the Phillips group.

The court case had primarily applied to the Ekofisk field. Valhall first came on stream in 1982, so the claim for refunded interest was not so large where it was concerned.

Petroleum Act prompts fresh legal action

Avgifter til besvær, økonomi og samfunn,

Avgifter til besvær, økonomi og samfunn,A new Petroleum Act which came into force on 1 July 1985 introduced certain changes to the way royalty was calculated, and these were given retroactive effect.

The government’s right to benefit financially by amending the licence terms for fields which had already been licensed was quickly questioned.

Exactly two years after the Act came in, Phillips, Elf, Esso, Amoco and Marathon filed two separate compensation claims against the Ministry of Petroleum and Energy on behalf of the government.

The companies, who held interests in Ekofisk, Heimdal, Frigg, Odin, Tor and Valhall, wanted to recover several tens of millions of kroner in alleged overpayment of royalty during 1985-87.

Several of them had victories over the government in the Norwegian legal system fresh in their memories, and were fairly confident of winning again.

For its part, the ministry rejected the claim because the Petroleum Act had been given retroactive effect by the Storting and the government had simply kept to the letter of the law.[REMOVE]Fotnote: NTB, 27 July 1987, “Oljeselskaper går til rettssak mot staten”.

The first lawsuit, known as the Valhall case, concerned a 1985 provision that royalty should be paid separately for oil and gas from the same field rather than collectively as before.

That meant losses on unprofitable gas production could not be set against the gross value of oil output. The oil companies claimed this was illegal and demanded compensation for their loss.

In the other suit, known as the Statfjord case, the companies sought to have royalty calculated on the value of the petroleum at the wellhead rather than, as specified in the new Act, at its shipment point.[REMOVE]Fotnote: NTB, 22 September 1992, “Staten med million-avgiftsforlik i Nordsjøen”.

“Negative royalty” – the Valhall case

The Valhall case was brought by the field’s licensees – Amoco Norway Oil Company, Amerada Hess Norge A/S, Enterprise Oil Norge Ltd and Norwegian Oil Consortium A/S & Co (Noco). They claimed a total of NOK 4 million in compensation.[REMOVE]Fotnote: NTB, 22 September 1992, “Staten med million-avgiftsforlik i Nordsjøen”.

Avgifter til besvær, økonomi og samfunn,

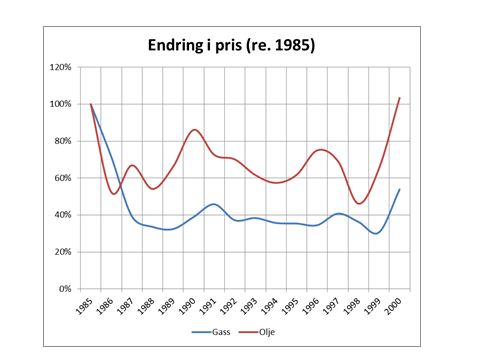

Avgifter til besvær, økonomi og samfunn,The question of whether royalty – eight to 16 per cent for oil and 12.5 per cent for gas – should be calculated separately or collectively became particularly relevant after gas prices fell dramatically in 1986.

It therefore cost more in some cases to produce gas than could be earned from selling it. The oil companies maintained that the consequent loss should be deductible from oil earnings when calculating royalty.

The government denied that this practice, known as “negative royalty”, was permitted. While the companies would pay no royalty on unprofitable gas production, they could not deduct such losses from the gross value of oil.

That accorded with the tax reliefs provided by the authorities in 1986, whereby oil companies bringing new fields on stream escaped royalty on gas production.

Amoco and the ministry discussed options for a compromise in this and other cases related to royalty. As explained below, this was achieved in 1996 and Amoco dropped this claim.[REMOVE]Fotnote: Proposition no 15 to the Storting (1996-97), Om endringar av løyvingar på statsbudsjettet for 1996 og andre saker under Nærings- og energidepartementet.

Date of calculating royalty – the Statfjord case

The amounts involved the Statfjord claim were considerably larger than in the Valhall dispute, and related to where in the process royalty should be calculated.

Once again, the oil companies questioned as a matter of principle the legality of changing licence terms once they had been established.

The Statfjord licensees took the ministry to court in the 1980s over a series of compensation claims which added up to NOK 441 million.

Amerada Hess Norge A/S accordingly wanted NOK 10 million, AmocoNoco Norway Oil Company NOK 10 million, Conoco Norway Inc NOK 86 million, Esso Exploration and Production Norway Inc NOK 92 million, Mobil Exploration Norway Inc NOK 132 million, A/S Norske Shell NOK 90 million, and Saga Petroleum A/S and Enterprise Oil Norge Ltd NOK 21 million.

As noted above, the oil companies wanted royalty to be calculated on the value of the petroleum at the wellhead – in other words, before processing – and not at the “shipment point for the production site”.

This wording, which replaced the former term “production site” in the 1972 regulations, was open to various interpretations and was a “technical disagreement” of great financial significance.

Calculating royalty at the wellhead, where the oil and gas emerged from the reservoir, provided opportunities for significantly larger tax deductions than if this was done at the shipment point – in other words, after the wellstream had reached the platform, been processed and was stored offshore for export.

To avoid a court case, the government reached an accord with the oil companies on a practical solution of the problem as early as 1978.

Costs related to transport – such as expenses for pipelines and so forth – could be deducted when calculating royalty, but not those associated with processing.

Called the Ekofisk solution, this meant that the calculation point was not a physical location but a functional position to establish the payment due.

Phillips sues again

When the new Petroleum Act came into force in 1985, the government changed its practice and dropped the Ekofisk solution. It now interpreted the shipment point on the field quite literally as the calculation basis.

The companies, who felt they had gone quite a long way in accepting the earlier compromise, reacted sharply to the change introduced by the new Act.

Avgifter til besvær, økonomi og samfunn,

Avgifter til besvær, økonomi og samfunn,This issue was particularly significant for the Ekofisk partners, who had made big investments in such upgrades as the breakwater wall around the field’s storage tank. With Ekofisk operator Phillips in the van, the licensees for Ekofisk, Frigg, Heimdal, Valhall and Odin took the government to court.

The companies argued that calculating royalty more stringently for older fields was inequitable – particularly when this payment was abolished for new fields as part of the tax reliefs introduced after the 1985-86 oil price slump.

Large sums were involved. Phillips Petroleum Company alone sued the government for around NOK 5 billion which it claimed to have overpaid in royalty.

The lawsuit was unwelcome to the government, and petroleum and energy minister Eivind Reiten issued what could be perceived as a threat to Phillips on 20 July 1990. He said his ministry would not look favourably on future licence applications from the company if it persisted with the claim.

As minister of petroleum and energy from 1989-90 in the non-socialist coalition headed by Conservative Jan P Syse, Eivind Reiten from the Centre Party urged the oil companies to compromise on the royalty issue – unless they wanted to end at the back of the queue for the award of new licences.

This legal action would be unfortunate for the government for several reasons. The ministry’s lawyers took the view that the companies had a very strong case, and feared they would win.

Furthermore, fighting the claim would tie up substantial resources in the ministry for many years. And avoiding a lengthy conflict with such a key player as Phillips was important.

All this put a premium on coming to terms. Nor, when the chips were down, was Phillips interested in a conflict and the company yielded to the pressure by accepting Reiten’s compromise.

This also involved retaining the earlier Ekofisk solution in principle after 1985. In addition, Phillips was allowed to deduct investment on Ekofisk after 1978 and received compensation of NOK 221 million.[REMOVE]Fotnote: Proposition no 95 to the Storting on implementing finance policy plans for 1990.

Having accepted a peaceful compromise, Phillips expected to be treated on an equal footing with all the other companies in future licensing rounds. And the government expected the other players to show a similar cooperative spirit in the negotiations.[REMOVE]Fotnote: Dagens Næringsliv , 20 July 1990, “Truet Phillips til å frafalle milliardkrav”.

Amoco compromise

The Amoco group’s turn to negotiate with the government came in 1996, when it reached a comprise with Ministry of Industry and Energy.[REMOVE]Fotnote: Proposition no 15 to the Storting (1996/97), Om endringar av løyvingar på statsbudsjettet for 1996 og andre saker under Nærings- og energidepartementet.

This settlement covered no less than five cases relating to royalty. These did not have clear links, and the ministry claimed it was not possible to agree “individual” solutions for each of them. Only an overall compromise could avoid a court hearing.

As noted above, the first of these issues was the “Valhall case” concerning negative royalty. The AmocoNoco group had been required to pay 12.5 per cent royalty on the gas produced from Valhall. But this output ran at a loss for a number of years, and the group argued that it could then deduct 12.5 per cent of the value of the gas from the royalty – a view the government rejected, and the group gave way.[REMOVE]Fotnote: Proposition no 15 to the Storting (1996/97), Om endringar av løyvingar på statsbudsjettet for 1996 og andre saker under Nærings- og energidepartementet.

The second case involved adjusting the lump sum mentioned above. A proviso of the “Valhall compromise” in 1991 was that the amount paid would be adjusted if royalty was not reduced to zero for both oil and gas from 1 January 1992.

Since royalty for oil was retained, it was clear that the lump sum had to be increased. But the 1996 compromise determined that this payment could not be upgraded in the future.

Cases three and four concerned a deduction for the area fee payable for block 3/4 in production licence 006, awarded to the AmocoNoco group in 1965, and for block 2/5.

According to the rules which applied when the award was made, the licensees could deduct the area fee in its entirety from royalty.

The fifth issue concerned a deduction from royalty for costs related to natural gas liquids (NGL), at a time when royalty had already been abolished for gas. Amoco maintained that the changes made to the Petroleum Act in 1985 did not apply to licences awarded in 1965. But it had to give way here, and accept that the 1985 provisions applied for future settlements.

Where this claim was concerned, Amoco accepted a ratio of 35/65 between oil and gas – in other words, a deduction was only allowed for 35 per cent of transport-related costs from producing condensate, although the company had to pay royalty for it.

The total value of the settlements in these five cases was put at NOK 199 million, compared with an initial claim of just over NOK 235 million from Amoco. The group also dropped other demands in the cases covered by the compromise.[REMOVE]Fotnote: Proposition no 15 to the Storting (1996/97), Om endringar av løyvingar på statsbudsjettet for 1996 og andre saker under Nærings- og energidepartementet.

As a conclusion to the whole story, royalty was abolished in its entirety for the Valhall field with effect from 1 January 2000.[REMOVE]Fotnote: Norwegian Official Reports (NOU) 2000:18, Skattlegging av petroleumsvirksomheten.

Act of 29 November 1996 No 72 relating to petroleum activities

Section 4-10 Area fee, production fee, etc.

The licensee shall pay a fee for a production licence, after expiry of the period stipulated pursuant to Section 3-9 first paragraph first sentence, calculated per square kilometre (area fee).

The licensee shall furthermore pay a fee calculated on the basis of the quantity and value of petroleum produced at the shipment point of the production area (production fee). With regard to petroleum which is injected, exchanged or stored prior to being delivered to be taken ashore or used for consumption, the production fee shall be calculated on the basis of the quantity and value of the petroleum at the shipment point for the original production area at the time when the petroleum according to contract is delivered to be taken ashore or used for consumption. Nevertheless, production fee shall not be paid for petroleum produced from deposits where the development plan is approved or where the requirement to submit a plan for development and operation is waived after 1 January 1986.

When granting a production licence, a non-recurring fee (cash bonus) may be levied and there may be stipulated a fee which shall be calculated on the basis of production volume (production bonus).

Up and down – and up again …Tax protest from Amoco