Tax protest from Amoco

“We’re willing to accept the negative consequences of saying that the financial terms in Norway aren’t good enough to justify applying for new interests in blocks in the ninth round,” Amoco public affairs manager Øyvind Kvaal said in August 1984.

The company was displeased with the Norwegian tax regime in general, and argued that the special tax levied on offshore players required an oil price of USD 40 per barrel – USD 10 above the 1984 level. It viewed the high tax rate as an obstacle to developing small fields such as Hod.[REMOVE]Fotnote: Aftenposten , 22 August 1984, “Nytt angrep på oljeskatten”.

Special tax imposed

A more detailed presentation of the way the offshore tax burden increased in several stages and with varying justifications is provided below.

When the first Petroleum Tax Act was passed by the Storting (parliament) in 1965, the Ministry of Finance took the view that the oil sector should be treated in the same way as other industry on land.

Ordinary corporation tax was levied at a rate of 50 per cent on profits. The main objective of oil policy at the time was to encourage maximum exploration to determine whether petroleum existed on the Norwegian continental shelf (NCS).

Offshore taxation was reassessed in the spring of 1972 after large quantities of oil and gas had been found in Ekofisk and this field had been brought on stream.

The tax rules were adjusted in part as a result of fiscal changes for limited companies a few years earlier. A progressive system was also introduced for calculating royalty on oil production.[REMOVE]Fotnote: Hanisch, Tore Jørgen, and Nerheim, Gunnar, Norsk Oljehistorie. Fra vantro til overmot . Bind 1, 1992, 420-421. (See the article on Rows over royalties.)

Amoco protesterer på skatten, økonomi og samfunn

Amoco protesterer på skatten, økonomi og samfunnThese adjustments were nevertheless moderate compared with the changes introduced three years later, in the wake of 1973-74 oil crisis which led to a quadrupling in global crude oil prices.

Israel had been in constant conflict with its Arab neighbours since the state was founded in 1948, and the Yom Kippur war broke out with Egypt, Jordan and Syria on 6 October 1973.

The USA supported the Israelis with military equipment, prompting the Organisation of the Petroleum Exporting Countries (Opec) to use oil for the first time as a political weapon.

Aimed at states backing Israel politically and militarily, the measures adopted included production cut-backs – with a ban on exports to certain nations – and a big rise in crude prices.

The boycott hit the western world hard and sparked a crisis in the world economy. Norway was also affected by fuel shortages, and took such steps as banning Sunday motoring.

While Norwegian shipping and shipbuilding suffered, however, the country’s oil production became more profitable. That combined with a nationalist mood after a 1972 referendum rejected joining the European Community.

One effect of this vote was a more radical attitude in government towards Norwegian oil taxation. A petroleum revenue committee (PIU) was established as early as 24 January 1974 to discuss state revenues from the industry.

The results of its work ended up as a key chapter in the seminal Report no 25 to the Storting (1973-1974) on the place of petroleum operations in Norwegian society.

This included the declaration that “Norway’s petroleum resources are the property of the Norwegian people and must benefit the whole society”.[REMOVE]Fotnote: Hanisch, Tore Jørgen, and Nerheim, Gunnar, Norsk Oljehistorie. Fra vantro til overmot . Bind 1, 1992, 419-426.

The price rise which accompanied the oil crisis meant that the government expected crude to continue to cost more in the future. Petroleum production from the NCS would thereby become far more profitable than previously expected.

The PIU accordingly took the view that Norway must conduct “a reassessment of the government’s attitude with regard to revenues from Norwegian petroleum activities on the NCS”.

Instead of treating the oil sector on a equal footing with other industry, calls were now made for a special tax which would only apply to petroleum operations.

In this context, the committee turned to the concept of economic rent.[REMOVE]Fotnote: For an explanation of the economic rent concept in Norwegian, see Norwegian Official Report (NOU) 2000: 18 Skattlegging av petroleumsvirksomheten. www.regjeringen.no/nb/dep/fin/dok/nouer/2000/nou-2000-18/13/2.html?id=359932 Income “which derives from the actual resource as such, and especially the unexpected new addition to this income” should fall to the owner of the resource – in other words, the Norwegian state.

The conclusion was that “the committee regards the justification for a special tax under the new price conditions as indisputable”.[REMOVE]Fotnote: Hanisch, Tore Jørgen, and Nerheim, Gunnar, Norsk Oljehistorie. Fra vantro til overmot . Bind 1, 1992, 427-428.

At the same time, it proposed that a new government body should calculate a notional price or value for oil and gas – known as the norm price.

The oil companies were shocked, to put it mildly. Phillips Petroleum, Shell, Agip and Norsk Hydro all reacted sharply, and maintained that binding agreements on tax rates – at least for a period – had been entered into in 1965.

Ably assisted by highly competent lawyers, the government emphasised for its part that the companies had only received production licences in 1965 on specific terms. The Storting could not bind itself then that a given tax rate would prevail in perpetuity.[REMOVE]Fotnote: Hanisch, Tore Jørgen, and Nerheim, Gunnar, Norsk Oljehistorie. Fra vantro til overmot . Bind 1, 1992, 429-433.

In protest, Chevron decided not to apply for new acreage in the next Norwegian licensing round. Amoco took even more tangible action by halting the planned development of South-East Tor.

This field was proven in 1972 and put into development in 1974, with a steel jacket (support structure) acquired for a platform and materials for its topside ordered.

After the finance minister reported in December 1974 on the new tax regime which was in the offing, further planning for the project was put on hold.

A press release was later issued to announce that South-East Tor, due to come on stream together with the Tor field in 1977, would not now be developed. It was so marginal that this would be uneconomic.[REMOVE]Fotnote: Øyvind Kvaal, articles in Amoco Viking. The discovery has since remained undeveloped.

Despite these protests, the new Petroleum Tax Act was passed on 13 June 1975. It comprised four elements, including the above-mentioned sliding scale from eight to 16 per cent for royalty.

In addition came ordinary corporation tax at the same 50.8 per cent rate as for land-based activities. The special tax comprised a levy of 25 per cent calculated on net income. Finally, the government acquired the power to set a norm price for petroleum calculated on the assumption that a free market existed.

The Act was adopted virtually unanimously, with the exception of the anti-tax Anders Lange’s Party, and boosted the marginal tax rate for the oil companies to a total of 75.8 per cent.

Tax burden follows oil prices

A new oil crisis occurred in 1979, following the Iranian revolution which deposed the Shah and brought Ayatollah Khomeini to power.

With memories of the first crisis still fresh, widespread hoarding of oil began worldwide, even though most countries had sufficient stocks to cover a brief production shortfall.

Prices were driven to even higher levels than in 1973-74, and peaked at USD 34 per barrel. They continued to rise after Iraq’s attack on Iran in 1980 and remained unusually high for the next five years.

This was beneficial for Norway as an oil producer, and new field developments were sanctioned on the NCS. But was it right for the oil companies to “skim the cream” from a boom market?

In line with the thinking which underpinned the 1975 Act, the special tax was increased in 1980. The government maintained that the rise in the economic rent from higher prices should fall to the state. This boosted the marginal tax rate for the oil companies to 85.8 per cent.

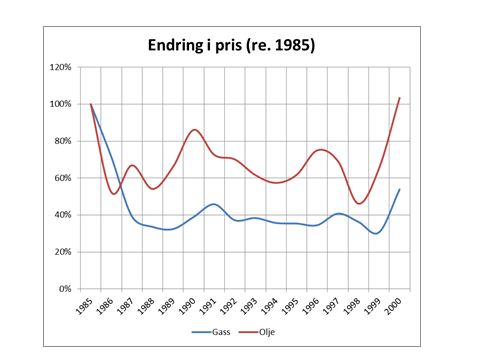

Oil prices began to decline in 1985, creating uncertainty about prospects for the petroleum sector. Amoco, for one, announced in February 1986 that development plans for Hod had been put on ice, and that no further investigation would be conducted on this oil and gas field while prices remained so low.

A rise in the price of oil or radical changes to the Norwegian tax regime were the only considerations which could persuade the AmocoNoco partners to change their minds.

Avgifter til besvær, økonomi og samfunn,

Avgifter til besvær, økonomi og samfunn,The spot price of North Sea (Brent Blend) oil reached a low of USD 10 per barrel on 2 April 1986. Nobody had expected it to fall so far.[REMOVE]Fotnote: Statistics Norway (SSB), Økonomiske analyser no 1 – 1987, 70.

A banking crisis, unrest in financial markets and a sharp fall in share prices on the Oslo Stock Exchange prompted the non-socialist coalition headed by Conservative premier Kaare Willoch to introduce austerity measures. But these failed to secure a majority in the Storting, and Labour leader Gro Harlem Brundtland formed a new government that May. The Norwegian krone was devalued and fiscal retrenchment taken even further.

To ensure that the NCS remained attractive to foreign oil companies, the Brundtland government presented a proposition (Bill) in August which introduced tax concessions for offshore exploration and production.

The requirement that foreign companies had to carry the costs of the state’s direct financial interest (SDFI) on the NCS was abolished for new production licences.

Royalty was also set to zero for future developments, and depreciation rules were amended to allow companies to write down spending on operating equipment from the first investment year.

Last but not least, the special tax was cut from 35 to 30 per cent.[REMOVE]Fotnote: Statistics Norway (SSB), Økonomiske analyser no 1 – 1987, 73. That reduced the marginal tax rate for the oil companies to 80.8 per cent.

Amoco sues over tax

Amoco Norway Oil Company was still not satisfied with Norway’s tax provisions, and initiated legal proceedings in the Oslo District Court against the Ministry of Finance in November 1988 over a disputed charge of about NOK 130 million.

On this occasion, the case did not concern tax rates but the opportunity for the companies to deduct interest charges on loans from their tax liability.

Amoco Norway’s operations were largely financed through loans raised by its parent company, which was registered in the US state of Delaware – regarded as a tax haven. (See the article on Financing the Valhall development.)

In its tax returns for 1982 to 1985, the Norwegian subsidiary had claimed deductions for interest paid to the parent company. The tax assessment authorities fully accepted that such charges could be deducted – but with one exception.

Hvordan bestemmes en utbygging?, forsidebilde, feltet, Amoco protesterer på skatten, økonomi og samfunn,

Hvordan bestemmes en utbygging?, forsidebilde, feltet, Amoco protesterer på skatten, økonomi og samfunn,Since Amoco Norway was to be regarded in tax terms as an independent company in relation to its parent, a certain minimum level of financing had to be treated as equity. This could not be deducted as interest on a loan.

Based on the equity calculated by the tax assessors, Amoco Norway was found to have underpaid its tax by NOK 130 million for 1982-85.

The interest deducted on the remainder of the loans was not in dispute. Amoco claimed for its part that the total loan must also be regarded as genuine for tax purposes.[REMOVE]Fotnote: Aftenposten , 5 November 1988, “Strid om oljeskatt for retten.”

In legal terms, the case concerned the application of section 54, paragraph 1 of the Petroleum Tax Act concerning “thin” capitalisation of companies producing petroleum.

This term applies to subsidiaries which operate with very limited equity. The legal issue was accordingly whether this section entitled the tax assessors to regard all or part of such loans as equity.

Amoco maintained that no grounds existed for doing this, with the effect that the sum which could be deducted for interest charges and currency losses was reduced.

The court, for its part, tried to assess what could be regarded as a “commercially reasonable and natural” capital structure.

Where Amoco Norway was concerned, equity accounted for only 1.7 per cent of its total capital – which did not represent a reasonable commercial relationship between debt and equity.

The company would not have been able to achieve such a high debt-to-equity ratio independently, and could not have obtained equally good terms by borrowing in an open market.

In legal terms, it had to be regarded in Norway as an independent entity. That made it reasonable for the tax assessors to calculate a higher equity, and base liability on that.

A number of purely legal issues were addressed by the court in its wide-ranging judgement, including the tax treaty between the USA and Norway and discrimination between Norwegian and foreign oil companies.

Amoco claimed it had been taxed more heavily than purely Norwegian-owned companies, which would in the event contravene the tax treaty. The court found no such discrimination had occurred.[REMOVE]Fotnote: Aftenposten , 27 January 1989, «Amoco tapte skattesak mot staten».

This judgement was a disappointment for Amoco Norway, since it upheld the power of the tax assessment authorities to regard part of its financing as equity. It had to pay not only the disputed NOK 130 million, but also the government’s legal costs.

A rich nation

Together the other oil companies, Amoco Norway could celebrate when the Storting approved a new tax regime in 1992 which cut their liability to the government.

The revised system involved a special tax of 50 per cent in addition to conventional corporation tax of 28 per cent. A production-based deduction from the special tax was replaced with an uplift related to investment. These changes almost returned the overall tax burden to the 1975 level.[REMOVE]Fotnote: Statistics Norway (SSB), Økonomiske analyser no 1 – 1993, 105.

Since Amoco Norway’s fiscal history ceased when it merged with BP in 1998, the changes in Norway’s petroleum tax regime which have occurred since then are not covered here.

Government revenues from petroleum taxation were relatively stable during the 1990s, and accounted for about five per cent of its overall income from direct and indirect taxes.

This proportion has risen sharply since 2000 to reach 14-23 per cent of the total. In 2010, petroleum tax totalled NOK 177 billion in 2011 value.

One reason for this growth was the restructuring undertaken in 2002, when the government established Petoro to take over the management of the SDFI and sold assets from this portfolio to the oil companies. More of the revenues from holdings disposed of in this way thereby derived from tax.

The bulk of petroleum taxation in Norway is paid by a handful of large companies – with Statoil in a special position.[REMOVE]Fotnote: Didrik Lund, “Erfaringer med rammevilkår for petroleumsproduksjon i Norge”, paper, 18 April 2012.

Revenues accruing to the state from the oil industry have made Norway a rich nation with a big sovereign wealth fund. This was established by the Storting in 1990 to secure the country’s future economic freedom of action.

Government income from the petroleum sector is transferred to the oil fund, which invests the money in foreign shares and bonds. The first allocations were made in 1995.

Since 2001, successive governments have subjected their use of oil cash in the domestic economy to the “fiscal rule”, which limits current drawings from the fund to the real rate of return on its investments.

That corresponds to about four per cent of the fund’s value at the start of a year, and aims to ensure a stable use of oil revenues for a long time to come.

Renamed the government pension fund – global in 2006, this “piggy bank” exceeded NOK 5 000 billion in December 2013. That corresponds to roughly NOK 1 million per Norwegian, and means that Norway can be regarded today as one of the world’s wealthiest nations.[REMOVE]Fotnote: Gjerde, Kristin Øye (2013), “Oljelandet og ny næring langs kysten”, 17.

Rows over royaltiesAmoco protesterer på skatten