Financing the Valhall development

Norwegian banks in an age of oil

Finansiering av utbyggingen,

Finansiering av utbyggingen,Oil financing was a new and highly interesting sector for Norwegian banks in the 1960s. Den norske Creditbank (DnC) was the country’s biggest, and the first to get involved in this business.

Its initial modest commitment occurred in 1967 as a shareholder in Syracuse Oils A/S, an oil company which had been established two years earlier with about half the shares in Norwegian hands.

This was at a time when petroleum had still not been discovered in the Norwegian North Sea. But DnC considered it a “national duty” to become involved in the new industry despite the high level of risk involved.

The bank already had broad experience of commitments in industry and shipping, with the latter sector in particular an international and highly capital-intensive business.

Oil exploration was nevertheless different, and on a larger scale. Getting involved early in this market, in order to learn and gain experience, was to prove profitable.

Once hydrocarbons had been discovered in Ekofisk, DnC also took a stake in Saga Petroleum forerunner Nocoto in 1971. But such direct commitments posed a dilemma – should the bank be a shareholder, or confine itself to financing exploration and production by others?

The conclusion was that DnC would not take direct holdings in oil companies, and it sold all such interests to Saga. But this early involvement in petroleum paid off to some extent.

With its own oil department and the expertise and experience gained as a shareholder, the bank was well equipped to become a source of finance for petroleum projects.

One of the first lessons DnC learnt was that this was a growth sector. Just before the shipping business was hit by a global crisis in 1973, Nils B Gulnes, the newly appointed head of the bank’s oil department and a former deputy director in the Ministry of Industry, noted that the same fate was unlikely to befall the petroleum industry.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 236-239.

Nor did it. The Yom Kippur War in the autumn of 1973 made oil and gas from the politically stable North Sea basin even more attractive.

And developments were queuing up on the Norwegian continental shelf (NCS): Ekofisk, Frigg, Statfjord and Valhall. Financing requirements for Norway’s offshore sector were clearly going to rise very sharply.

Traditionally, international oil companies had made only limited use of loan capital. They had relied on internal borrowing from their parent corporation at low interest rates. But expensive offshore developments made them increasingly reliant on external funding.

While outside borrowing had traditionally accounted for about 10 per cent of capital in the petroleum industry, the proportion had risen to more than 30 per cent by the early 1970s.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 240.

This provided a fast-growing market for credit institutions, but the funding required represented a completely different order of magnitude than Norwegian banks were used to.

In reality, financing assignments for field developments were too big for any individual bank to tackle alone. They had in every case to be handled by international lending consortia.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 240.

Finansiering av utbyggingen,

Finansiering av utbyggingen,DnC took the initiative in 1972 – the same year it sold its oil company interests to Saga – on establishing the Norwegian Bank Group for Petroleum Financing. Those invited to participate were Bergens Privatbank, Christiania Bank og Kreditkasse, Andresens Bank and Fellesbanken.

The object was to participate in the development and production of petroleum deposits as well as landing via pipelines, terminals and other associated installations. Activities were to be related to the NCS and Norwegian territory.

Construction of the pipelines from Ekofisk to the UK and Germany was the first substantial financing assignment taken on by the group.

Loans were also provided for the Frigg gas field development, but concerns began to surface after the support structure for one of its platforms was wrecked during installation. All the banks except Bergens Privatbank pulled out, and a French bank had to ride to the rescue.

In other words, the bank group broke apart. It provides an example of the trial-and-error approach taken to petroleum financing at this time. The various banks subsequently preferred to operate independently.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 241.

AmocoNoco-gruppen søker konsesjon, Finansiering av utbyggingen

AmocoNoco-gruppen søker konsesjon, Finansiering av utbyggingenDnC’s oil department developed a strategy in 1973-74 which sought to make the bank as much an ”oil financing broker [as] an oil bank participating with its own funds”.

The aim was to become an expert in drawing up loan agreements. It was explicitly stated that, to acquire a solid reputation, DnC had to be willing to operate worldwide in the same way as in the shipping market.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 243.

Amoco involves Norway’s banking sector

Developing Valhall was initially estimated to cost USD 652.7 million in 1976.[REMOVE]Fotnote: Kostnadsanalysen norsk kontinentalsokkel. Three years later, that figure had risen to USD 822 million.[REMOVE]Fotnote: Aftenposten, 9 March 1979, “Milepæl for norsk bankvesen”.

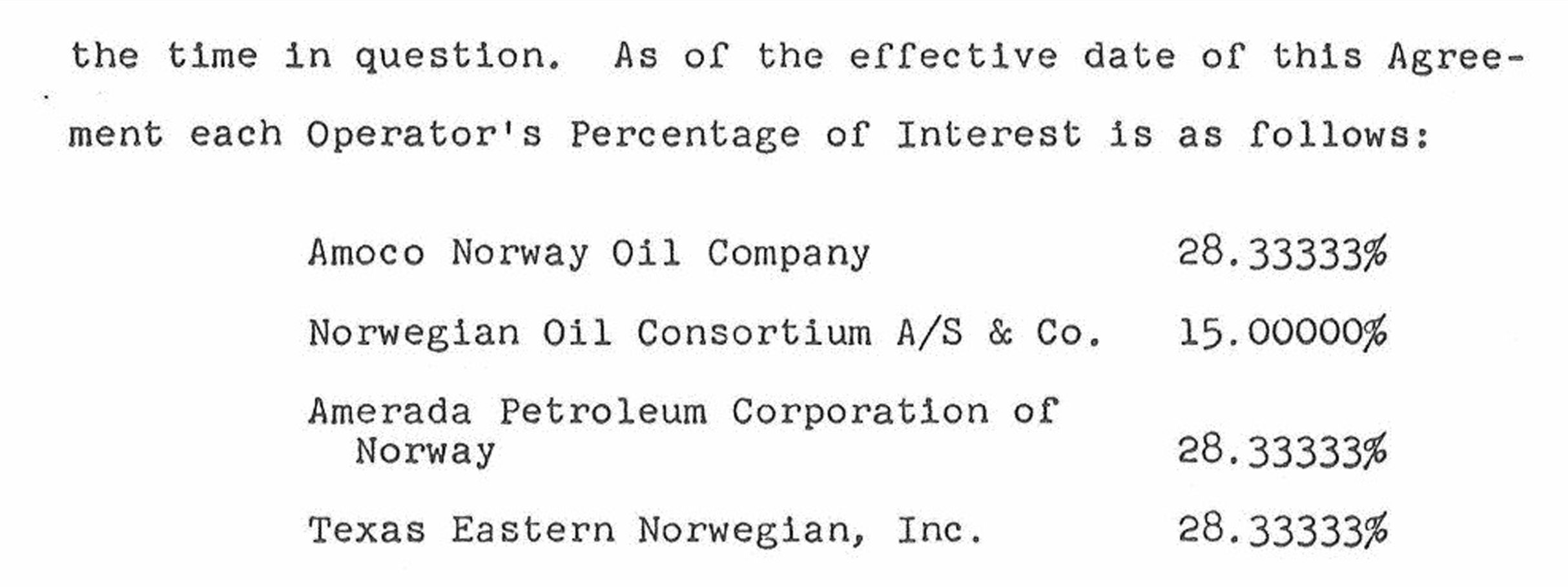

US partners Amoco, Amerada Hess and Texas Eastern each held 28.33 per cent of the field, while the Noco limited partnership had 15 per cent.

The latter was owned at the time by 16 Norwegian industrial, shipping and insurance companies, having been established in 1965 with 20 partners. (See the article on Norwegian interests get involved offshore.)

Amoco sought in 1977 to raise USD 150 million in the loan market to meet about 65 per cent of its share of the development bill.

DnC was one of five petroleum banks which wanted to produce a financing package, and its strategy proved wholly successful when it was chosen as agent and one of two lead coordinators.

This assignment was a milestone – not only because a Norwegian bank was selected to manage Amoco’s big loan but also because the latter was innovative. Collateral was tied to the progress of the actual project rather than the financial status of the borrower.

DnC was proud that, despite being such a small player in an international context, it was chosen as a coordinator. This reflected its knowledge of Norwegian political and legal conditions related to offshore operations in the North Sea, which meant it was better able than foreign banks to judge the financial burden which the Valhall field could bear.

“This must be regarded as a big Norwegian foreign delivery of goods or services,” said DnC’s Borger A Lenth. “It supplies knowledge to a market which is perhaps the only remaining free market in the world. This is a free-for-all.”

Amoco took 18 months to choose its banks through a selection process which left it with DnC and Morgan Guaranty Trust, a New York financing institution with a long history and project finance experience from a number of countries.

The upshot was a collaboration whereby these two banks were the lead coordinators – in other words, responsible for managing the loan.[REMOVE]Fotnote: Aftenposten, 9 March 1979, “Milepæl for norsk bankvesen”.

DnC was to provide USD 10 million of the loan, with about half this amount coming from its own resources and the rest from other European banks.

In other words, the Norwegian bank was fairly uninteresting as a source of funds. What made it interesting was its knowledge. The deal was signed in March 1979.

“Funding for such a large project would normally be decided in the big financial markets of London and New York,” observed Lenth. “We would then have had the same sort of subordinate role [Norway] played in the [mediaeval] Hanseatic era.”

The knowledge concerned related in part to the risk associated with government rights under the licences, such as rationing North Sea production or changes to tax terms or royalties.

DnC’s oil department used both in-house and external lawyers and experts in international financing for this work. It could thereby present the operating parameters for the oil companies to the international banking market, which was not particularly well informed about these.

The USD 150 million loan of 1979 was renegotiated in February 1982 and increased to USD 225 million.[REMOVE]Fotnote: Aftenposten , 10 February 1982, “225 mill. dollar til Amoco”. By then, Valhall’s development was two years behind schedule and much more expensive than first estimated. [REMOVE]Fotnote: Stavanger Aftenblad , 2 October 1982, “Valhall i produksjon to år etter planen”.

Relating repayment of the loan to the field’s ability to produce was advantageous for the oil companies. The drawback was that it cost rather more because the banks had to be compensated for accepting such a risk.[REMOVE]Fotnote: Stavanger Aftenblad , 2 October 1982, “Valhall i produksjon to år etter planen”.

Project loans of this kind were a flexible solution tailored for the oil industry. That flexibility reflected the uncertainty. In reality, more of the latter was transferred to the banks – who lacked, for example, fixed guarantees on the repayment schedule.

While large, financially strong companies could demand a low interest rate, the less well-established players who posed a bigger risk had to pay higher rates. The latter had a particular need for the flexibility provided by the system of “self-liquidating” project loans.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 248-249.

Noco borrows from Sweden in exchange for oil

When Valhall came to be financed, Noco and its partners had already earned their first kroner from the nearby Tor field. The consortium had a four-per-cent stake in the latter.

It had secured its share of Tor’s development costs without borrowing – in other words, NOK 45-50 million from a total bill of NOK 1.2 billion.

A start to production from this field in June 1978 provided welcome revenues. Tor contributed NOK 370 million to fund Noco’s operations and the initial investment on Valhall in 1978-81.

This nevertheless fell well short of the capital required for developing Valhall A.[REMOVE]Fotnote: E-mail from Leif Dons, 28 January 2014. That was put at NOK 4 billion in 1979, with Noco’s 15 per cent share totalling roughly NOK 600 million.

A solution was first sought in Sweden, with Noco entering into a financing agreement in early 1979 with Svenska Petroleum AB which provided USD 100 million from the international capital market under a Swedish government guarantee.[REMOVE]Fotnote: VG , 11 September 1979, “Søta bror får Ekofisk-andel” and Stavanger Aftenblad , 12 May 1979, “Svenska Petroleum med i Nordsjøen”. The collateral provided was Noco’s licence rights and installations on Valhall.

In addition to the normal bank interest rate, the consortium also accepted a “liquid charge” (royalty) of 2.5 per cent on its production from Tor and Valhall over the producing life of these fields.

Noco also agreed to transfer a 10 per cent holding in block 2/9 near Valhall, where the consortium’s interest was 25 per cent, to the Swedish oil company. This form of financing was chosen so that the partners in Noco did not have to put up collateral.[REMOVE]Fotnote: Noco annual report, 1979.

Finansiering av utbyggingen, forsidebile, økonomi,

Finansiering av utbyggingen, forsidebile, økonomi,Svenska Petroleum’s object was to secure oil supplies for Sweden. Noco’s undertaking to deliver its whole share of output from Tor and Valhall over their producing lives was therefore the fundamental condition for the deal.

The oil was to be sold at a market price established through quarterly price negotiations.[REMOVE]Fotnote: E-mail from Leif Dons, 28 January 2014. When the agreement was signed, the quantity involved was expected to total six million tonnes.

So the Swedes were not brought into the Norwegian oil sector through the better-known attempt to establish a deal with Volvo, but by Valhall. Svenska Petroleum became involved in North Sea activities, while ensuring crude deliveries to Sweden.

Noco loan secured on the field

Estimates of total development costs for Valhall rose year by year, and increased from NOK 4 billion to NOK 7 billion between 1979 and 1981.

Noco’s 15 per cent share of the latter amount was more than NOK 1 billion. Since its Swedish loan failed to cover the increase, the consortium invited a number of banks to submit offers for new financing.

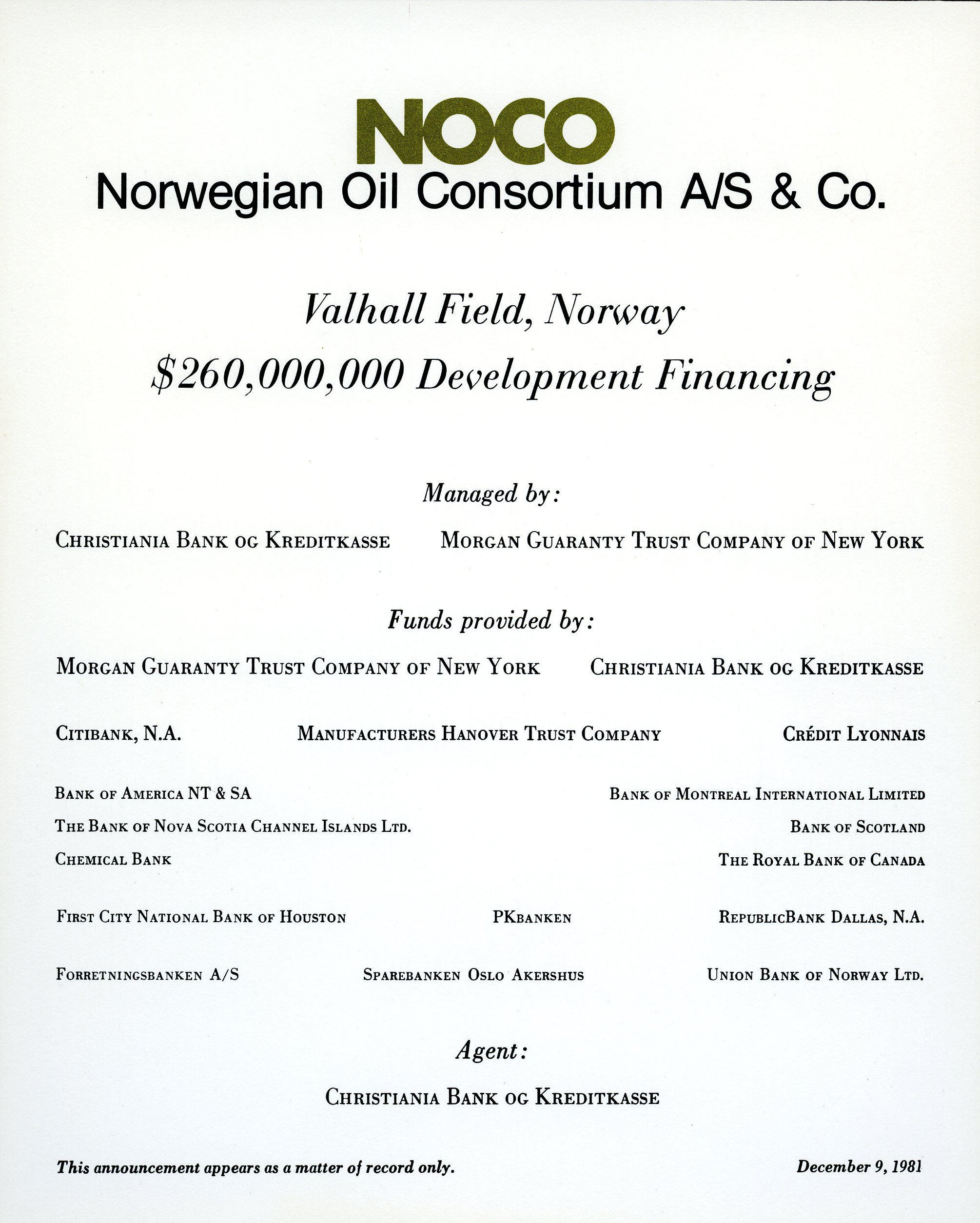

A contract with a loan framework of USD 260 million, corresponding to NOK 1 313 million, was signed on 11 October 1981 in Oslo by Noco and 17 Norwegian and foreign banks.

Christiania Bank and Morgan Guaranty Trust Company of New York, which was also involved in providing loans to Amoco, coordinated the syndicate on this occasion.

They accounted for about a quarter of the loan, while other participants hailed from Sweden, the UK, France and Canada as well as Norway and the USA.[REMOVE]Fotnote: Norwegian banks involved included Forretningsbanken and Sparebanken Oslo Akershus.

The loan covered both redemption of the loan from Sweden and continued financing of the Valhall and Tor developments.[REMOVE]Fotnote: Stavanger Aftenblad , 19 January 1982, “Large loan”. It ranked as one of the largest deals of its kind in Norway.

Christiania Bank thereby strengthened its involvement in the oil sector, where DnC had so far played the leading role among Norwegian banks.

This was a typical project loan, with floating interest charges tied to the London interbank offered rate (Libor). The latter lay between 12 and 20 per cent in 1980.

The banks primarily made their profit through the margin – normally one per cent – they charged in addition to Libor on the outstanding balance. That also applied with the Noco loan.

Instalments on the loan were to be adjusted to the revenues Noco could expect to receive when Valhall came on stream in 1982.

As part of this refinancing, Noco sought to cancel its commitment to pay the “liquid charge” or royalty to Svenska Petroleum.

This issue went to arbitration, but remained unresolved until a compromise in 1989 through a new sales deal with Sweden’s OK Petroleum AS, which had then taken over from Svenska Petroleum.[REMOVE]Fotnote: E-mail from Leif Dons, 28 January 2014.

Noco – liten men attraktiv, Finansiering av utbyggingen

Noco – liten men attraktiv, Finansiering av utbyggingenTor Moursund, chief executive of Christiania Bank, described the USD 260 million loan as a milestone in terms of both size and type for his company and for the Norwegian banking sector.

The collateral differed from conventional practice in Norway. In principle, it rested on sufficient quantities of oil and gas flowing from the wells at prices which covered costs, interest charges and instalments.

Should the geological and technical calculations for Valhall prove wrong, the banks had to bear the risk. They held a mortgage on the field and, as this had never been done before, a new official register had to be established.

That represented a significant difference from the loan raised by Amoco in 1979, where the risk lay with the oil company if the field failed to contain the expected quantity of petroleum.[REMOVE]Fotnote: E-mail from Leif Dons, 23 January 2014.

According to Carl W Carstens, Noco’s managing director, acceptance of the risk by the banks was crucial. it removed the financial responsibility from the consortium’s partners.

Vice president Gunnar Frognes at Christiania Bank, the architect of the loan, said that his bank felt comfortable with the balance between risk and reward. He reported that the banking world had shown great interest in joining the syndicate.

“Our organisation of this loan has allowed us to emulate the world’s leading banks with regard to this very complex and risky form of financing,” said Moursund.

The banks had investigated the technical, legal and financial prospects for Valhall and tailored the loan to Norwegian conditions.

Both the Bank of Norway and the Ministry of Petroleum and Energy had been involved in the development of the agreements which made up the loan package.[REMOVE]Fotnote: Aftenposten , 12 October 1981, “Milliardlån til norsk sokkel”.

Price slump makes banks nervous

Finansiering av utbyggingen,

Finansiering av utbyggingen,Vidkunn Hveding, Norway’s petroleum and energy minister, also praised the participating banks for displaying inventiveness and a willingness to think along new lines with this financing package.

“The innovation with this type of loan is that banks and resources are more directly coupled,” he said. “That should make it easier to secure loans for companies with few employees, for example, but with proven resources in hand.”[REMOVE]Fotnote: Aftenposten , 12 October 1981, “Milliardlån til norsk sokkel”. The description fitted Noco perfectly.

But the harmony which had prevailed when the loan deal was signed declined after Valhall ran into problems with the wells in its chalk reservoir once production started.

Finding solutions for this took time, but most of the wells which had been blocked by chalk intrusion had been cleaned and brought back into production by early 1986.

That meant a total of 17 wells were on stream. (See the article on The reservoir .) But problems of a completely different character now emerged.

Oil prices had dropped from USD 40 per barrel when the contract was signed to USD 20 in the first quarter of 1986, and sank further to USD 12 by the end of the year.

Since it was tied to cash flow in the company, redemption of the USD 260 million loan was thereby further delayed – even though the outstanding balance fell from USD 143 million to USD 113 million over the year.

This was much slower than expected. Plans called for the loan to be repaid by 30 November 1988. That looked fairly unlikely if oil prices remained at the same low level.[REMOVE]Fotnote: Noco annual report, 1986.

The banks which had lent money to Noco began to get nervous, and managing director Leif Dons was called on one occasion to a meeting with Morgan Guaranty Trust Company in New York. He was asked to request Noco’s owners to guarantee the rest of the loan.

Dons responded by asking Morgan Guaranty where this was stated in the contract, and rejected the request. The bank refused to give up and applied pressure, but to no avail.

Taking the view that he had the law on his side, Dons rose and left the meeting. Once back in Oslo, he was concerned about how Fred Olsen, Noco’s chair from March 1987, would react. But the latter felt that Dons had acted appropriately in refusing to make concessions to the banks. An agreement was an agreement. Moreover, securing such guarantees from Noco’s partners would be virtually impossible.[REMOVE]Fotnote: Leif Dons in conversation with Kristin Øye Gjerde, 22 January 2014.

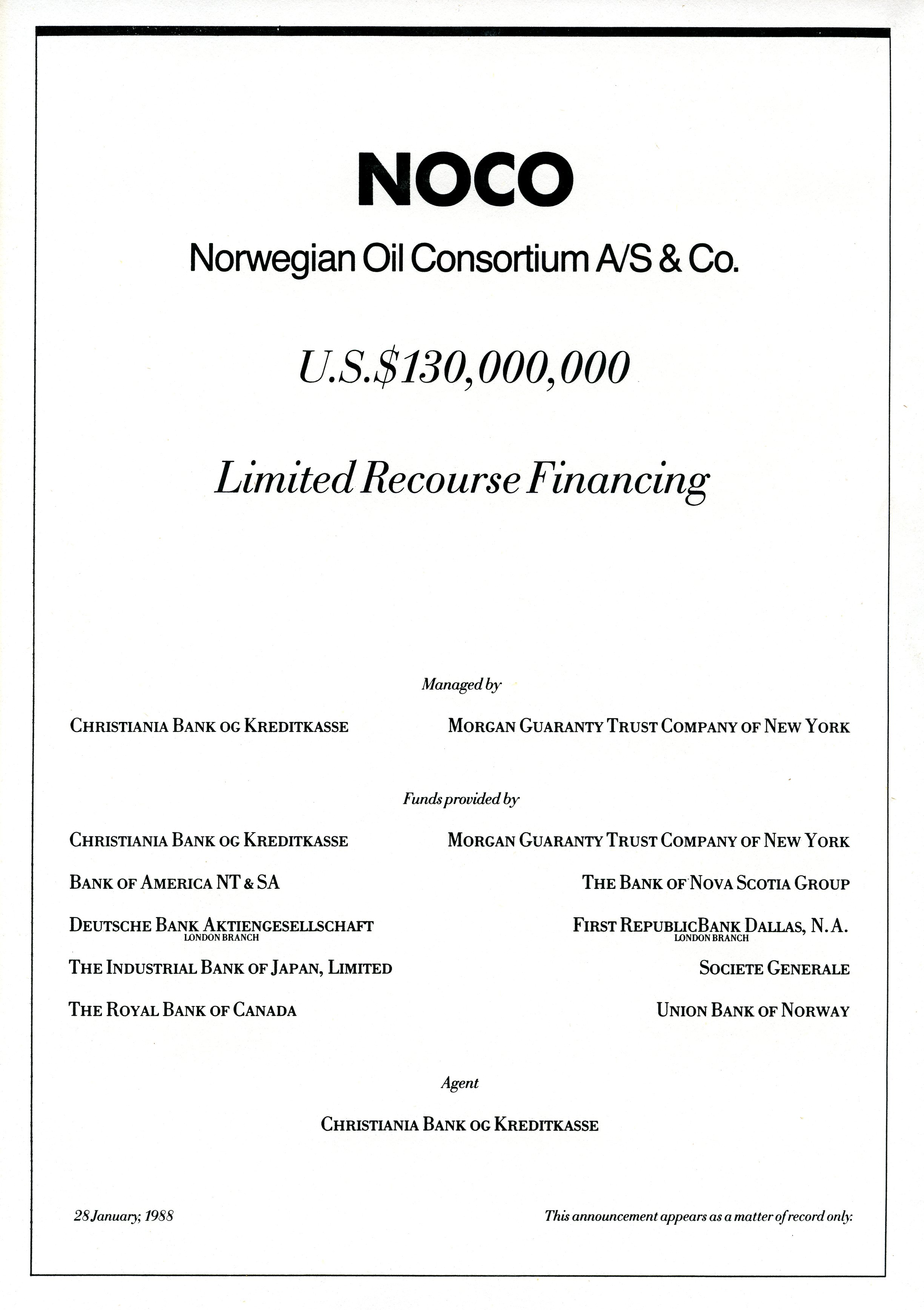

Finansiering av utbyggingen,

Finansiering av utbyggingen,The Noco board nevertheless had to ensure long-term financing. Although the loan was further reduced to USD 96 million in 1987, it remained a long way short of being redeemed.

Christiania Bank and Morgan Guaranty were mandated to refinance the loan in November 1987, and a new agreement totalling USD 130 million was signed on 28 January 1988.

Collateral was again provided by the company’s licences and producing fields.[REMOVE]Fotnote: Noco annual report, 1987. With oil prices rising, redemption went smoothly and Noco could announce as early as the annual report for 1989 that liquidity was good, the partners would receive a dividend of USD 9 million, and redeeming the loan by the agreed deadline of 1992 posed no problem.[REMOVE]Fotnote: Noco annual report, 1989. But the banks appeared to have learnt a lesson. Sitting with the risk for an oil field was not particularly good business when crude prices were at rock bottom.

As far as is known, these agreements with Christiania Bank and Morgan Guaranty accordingly became the first and last of their kind.[REMOVE]Fotnote: Leif Dons in conversation with Kristin Øye Gjerde, 22 January 2014.

Texas Eastern goes it alone

The most anonymous company among the Valhall licensees was Texas Eastern Norwegian Inc, a subsidiary of Houston-based Texas Eastern Corporation.

Established in 1947 as Texas Eastern Transmission Corporation, it worked mainly in the USA with pipeline transport of gas and oil, refining, petrol sales and property development.[REMOVE]Fotnote: Noco annual report, 1986.

The company began to show an interest in the North Sea during the 1960s. Both as a participant in the AmocoNoco group and in other consortia, it secured interests in a number of licences on the NCS which involved both exploration and production.

Texas Eastern had holdings in Valhall, Tor, Statfjord and Murchison as well as Hod and Snorre. Since it had not specialised in oil production, however, the company held no operatorships.[REMOVE]Fotnote: Noco annual report, 1986.

Not much was written about Texas Eastern in the Norwegian press during the 1970s and 1980s. It received revenues from 1978 as a licensee in Tor, but is likely to have secured financing for Valhall and other projects through loans from the US parent.

Texas Eastern’s position as an energy company was strengthened by acquiring Petrolane Inc in 1984. Not being an operator, however, the company was itself seen as a takeover candidate.

It was acquired in 1989 by Enterprise Oil Norway, a subsidiary of Britain’s Enterprise Oil which was established solely to continue Texas Eastern Norwegian Inc’s operations.[REMOVE]Fotnote: NTB, 13 March 1991, “Resultatframgang for Enterprise Oil Norge”. Enterprise was established in 1982 by the UK government to handle the offshore oil exploration and production interests of the British Gas Corporation. Privatised and listed on the stock exchange in 1984, it was taken over in 2002 by Royal Dutch Shell for GBP 3.5 billion. http://www.dn.no/arkiv/article27485.ece

Amerada Hess borrows in Norwegian kroner

Amerada Hess also borrowed money in Norway for the Valhall development, where it had a 28.1 per cent holding. This US oil company was based in New York and was the result of a merger.

Founded by British oil entrepreneur Lord Cowdray in 1919, Amerada ranked as a significant oil producer in North America. Hess was established by Leon Hess in 1933, and had specialised in refining and sale of petroleum products.

The pair complemented each other, and merged in 1969 to create Amerada Hess Corporation. Activity expanded, and the company was interested in both British and Norwegian North Sea sectors.

Amerada’s involvement from 1965 as a licensee in both Tor and Valhall on the NCS made a substantial contribution to this portfolio.[REMOVE]Fotnote: Amerada Hess changed its name to Hess Corporation in May 2006. Source: Amerada Hess website.

Through its Norwegian arm, Amerada Hess became the first borrower to take advantage of a new scheme for raising loans in Norwegian kroner to finance offshore operations on the NCS.

The NOK 400 million loan was arranged by DnC, which contributed to the funding package as well as acting as its agent. Other participants were Sparebanken Oslo Akershus, Forretningsbanken, Nordlandsbank, Rogalandsbanken and Vestlandsbanken.

This line-up shows that Norway’s smaller banking players benefited when the financing requirements became too large for the country’s biggest banks.

DnC was solidly established in this market, and had been working for some time on designing the contract for the Amerada Hess loan and its interest rate provisions.

Similar terms were used for other funding packages of the same type, including o

Norwegian banks could expand their lending to operations on the NCS because the government allowed them in 1982 to make kroner loans for such activities which did not count towards their compulsory reserve (primary capital) requirements.ne of NOK 1 billion for Statoil. Lending money to the latter was fairly safe, since it had a government guarantee.

This was because these loans helped to suck liquidity out of the mainland economy without being tied up in government bonds offering low interest rates. They thereby provided an alternative to higher primary capital requirements, which paid better for the banks.

An overall framework for NOK 3 billion had been established for such loans for 1982, of which NOK 1.4 billion was used by Amerada Hess and Statoil.

A new feature of this loan was that its interest charges were linked to the Oslo interbank offered rate – defined as the rate paid for krone deposits in Oslo’s forward currency market.

This meant that interest on the loan was determined by the market, in the same way as borrowings in foreign currencies tied to Libor.

Senior executive Stein Wessel Aas in DnC described this as “an important step towards developing a more differentiated offer to the market for the krone, both at home and abroad.”[REMOVE]Fotnote: Aftenposten , 10 May 1982, “Amerada Hess med ny type kronelån”.

Calculated risk

As noted above, both Christiania Bank and DnC had found a niche in petroleum financing where they could collaborate on an equal footing and compete effectively with the big international banks.

That particularly reflected the local knowledge of field developments on the NCS which Norwegian banks could acquire more easily than their foreign counterparts.

Arranging loans was more important than the ability to lend, and securing the position of agents meant a lot financially for the Norwegian banks.

They thereby got to be in charge of large payment flows which provided a built-in profit. But a petroleum bank also had other ways of making money.

All the companies operating on the NCS needed working accounts with a Norwegian bank, and these involved very substantial transactions. Tax payments alone represented big cash flows.

Bergen Bank and Rogalandsbanken, both based in western Norway, made a particularly strong commitment to this market, but DnC and Christiania Bank also moved into it.[REMOVE]Fotnote: Sejersted, Francis, ed (1982), En storbank i blandingsøkonomien. Den norske Creditbank 1957–1982 , 253–255.

The 1970s and 1980s were a time of trial and error for the Norwegian banks in their efforts to build expertise in an oil market characterised by taking big gambles.

Assessing the profitability of field developments was a risky business, which rested on the assumption that the oil and gas reserves involved had been accurately estimated.

Questions the banks had to ask included whether the technology was sufficient for the challenges faced, how oil prices and government policies on licences and taxes might develop, and what impact international political and economic developments could have.

The pitfalls were many and much could go wrong – but this sector also offered big opportunities for making profits.

Valhall orders for crisis-hit yardsNoco – small but attractive